Pakistani government plans to cancel industrial sector subsidies on gas rates. Previously, gas rates for industrial sectors were $6.5 per unit. This step is only the first part of a three-phased tariff rationalization plan of the government of Pakistan. The government has taken this step because of supply shortages and the unsustainable average cost of gas. Captive power plants are also included in the Industrial sector.

Ministry of Energy has sent a summary to the federal cabinet to cancel all the subsidized gas rates to the industrial sector, the statement said by the senior government official. He also said that a cabinet meeting is scheduled for today, where this issue will be discussed.

“We cannot ensure cheap gas to the industry when there is an extreme shortage and imported gas is five times expensive,” the official said. “We have been persuading them [industry] to shift to electricity which the government is ready to provide at lower rates, but there are no more options. Those unable to switch over would have to pay the full cost of supply.”

The official also said the average price of local gas is prescribed to be around Pkr645/unit (million British thermal units). And the delivered costing price of LNG (liquefied natural gas) cargoes is gone above Pkr 5,000/unit. And the average LNG sale price in October was about Pkr 2,730/unit.

The Government of Pakistan has offered Gas to the industry at a flat rate of $6.5 per unit. Along with the electricity tariff of 9.5 cents per unit. Other than that the incentive package of Rs12.96 per unit for incremental consumption. The gas shortage within the network is now exceeding at an alarming rate with 400-500 million cubic feet per day.

Download APTMA Management Report – October 2021

APTMA is the premier association of the textile sector and the largest association of Pakistan, representing spinning, weaving and composite mills. APTMA is primarily responsible for protecting and promoting the interests of the textile industry. The Association actively works to resolve issues pertaining to trade, commerce and manufacture of textiles, with a particular focus on cotton. The monthly APTMA Management Report is being circulated to share important statistics and information so as to ensure consistency across the textile industry.

Gas Supply & Competitive Energy Tariffs

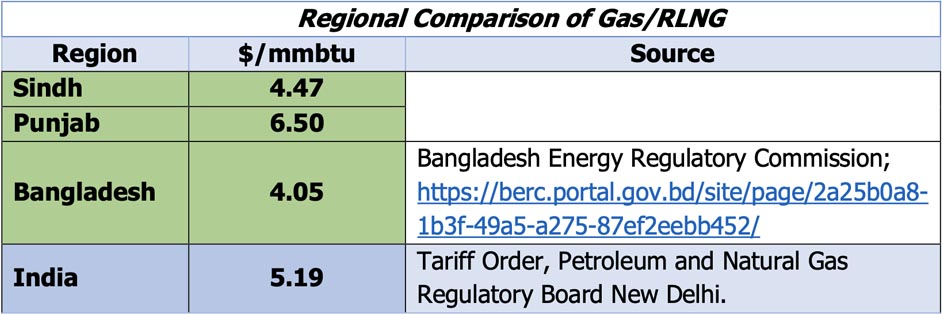

Gas / RLNG rate for Export Oriented Units (EOUs) in KPK and Sindh is currently Rs 760 ($ 4.47) and for Punjab is Rs 1105 ($6.5) / MMBTU. It is now proposed to increase the Gas / RLNG rate for Punjab from Rs 1105 ($6.5) to Rs 1530 ($9) / mmbtu. The 39 percent increase in gas / RLNG rate would be disastrous for industry (70%) located in Punjab. This would be highly discriminatory and unworkable.

An increase of $ 2.5 / mmbtu would result in a 3-4 percent rise in the final cost. As the textile industry operates on very slim margins of 3 to 4%, increasing the cost for 70% of the Industry will therefore render it uncompetitive and unserviceable which will lead to large scale unemployment and closures.

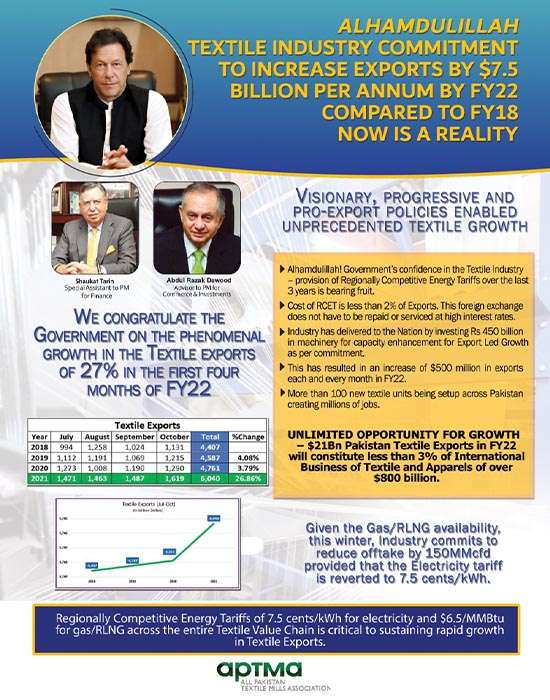

The Regionally Competitive Energy Tariff (RCET) provided by the current government over the past 3 years has yielded outstanding results. Industry has delivered to the nation by investing Rs 450 billion in machinery for capacity enhancement for export led growth as per commitment. This has resulted in an increase of $ 500 million in exports each and every month in FY22 so far. 100 new textile units are being set up across Pakistan, 90 percent of them in Punjab creating millions of jobs.

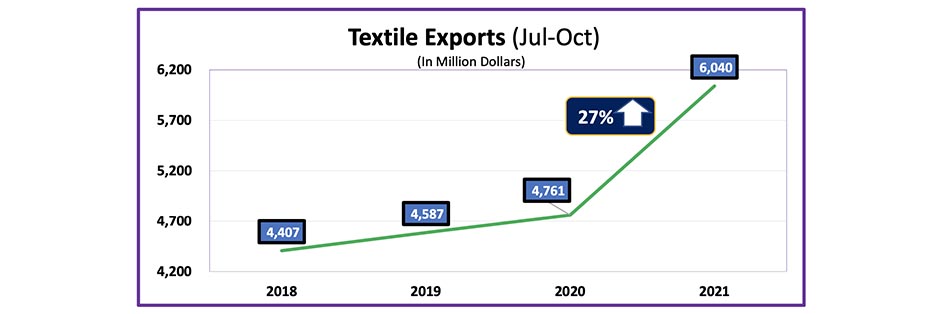

The textile industry’s commitment to increase exports by $7.5 billion by fiscal year 2021-22 over fiscal year 2017-18 has become a reality. The current government’s visionary, progressive, and pro-export policies have enabled unprecedented textile export growth. Textile exports increased by 27 percent in the first four months of the current fiscal year.

There is practically no subsidy on energy as competitive pricing is the right of any export sector as export sector has to compete on a pure cost/ quality basis in international competitive markets.

Given the Gas / RLNG availability, this winter, industry commits to reduce offtake by up to 100 mmcfd.

- Electricity tariff is reverted to 7.5 cents / kwh.

- Our alternative proposal for power generation is implemented and c) Fuel oil supply to export sector assured.

For the sake of just $ 38 million ($2.517090), the exceptional progress achieved in textile sector, increase in exports, investment and job creation is being jeopardized and the tremendous achievement of this government nullified.

Power Sector – Alternative Power Generation Plan to decrease use of RLNG/Gas

The current plan this winter relies on dependence on the three RLNG fuelled Punjab RLNG CPPs and shutting of FO based generation of Muzaffargarh and Jamshoro (with least capacity payments). FO based power plants can be put in service on the immediate basis. 1650 MW KAPCO is mostly dual fired, hence provision of FO for it would add another 1000- 1400 MW (minimum capacity charges) to the generation. This would further reduce the requirement of RLNG for the Power Sector. Similarly, other hi-efficiency FO based 2002 Policy IPPs viz. Attack, Nishat , Nishat Chunian, Atlas , Hub Narowal , Liberty Tech etc would easily add a further 1500 MW of again low capacity charges generation to the system . Consequently, due quantities of FO have to the arranged.

This 2000 MW FO based generation can save on the requirement of RLNG/GAS during the period December 2021 till end Feb 2022, besides providing power at 60% of cost.

Tube well loads can be easily managed by strict monitoring through AMI facility available in major tube well areas. Supply to tube wells can be only made available during sowing times and in limited time periods. This will arrange for reduction in such loads by 500 – 800 MWs during various periods – resulting in load management and less expenditure on generation. However, it will need strict monitoring by the relevant DISCO staff and higher management.

Improvement in the supply quality to Industry at special rates – allowing more usage against the present constraints. This will again result in some reduction in the gas demand.

As supply quality is below par hence most industry even cannot draw on their full sanctioned loads – in case of need. Otherwise too a total of 93 applications for EOL (extension of load) are pending with the various DISCOs. These should have been taken up by the DISCOs on immediate basis. Full info of such pendency has already been shared by APTMA with the PD. Now the least that can be done is to allow extra usage by these applicants up to 5 MW (if the existing infra-structure allows) without any check.

General Comments

As many as nearly 700,000 applications for new connections were pending up to 30/6/2021. This figure has bloated to above one million at the end of October 2021 for all DISCOs and the K-ELECT, due to the following reasons.

Non- purchase of needed material by DISCOs during the last six months, quoting indecisiveness of BODs etc. No pressure to provide supply to applicants. Incentive not to provide connections as seemingly more load / customers is considered as more loss.

Conclusion

This has resulted in non-use of at least 800 MW of demand and ensuing reduction in the burden of capacity charges.

Recovery of anything between Rs 300-500 billion in the coming six months out of the nearly Rs 1.5 trillion of default is possible through concerted efforts by the DISCOs under the supervision of the Power Division. Incidentally, APTMA has already shared such a draft plan with the PD. This level of extra recovery will assist the GoP to even contemplate some reduction in the ever-increasing power tariffs and cover for any possible extra cost of import of winter RLNG.